The RCJ provides RSS

feeds from well-respected news organizations, giving

our readers a convenient

portal through which to stay abreast of world

events and issues. Use the links provided. The

following are on the RCJ Front Page Report homepage

(scroll both columns to the right).

ATWOOD - "A Toiler's Weird Odyssey of Deliverance"-AVAILABLE

NOW FOR KINDLE (INCLUDING KINDLE COMPUTER APPS) FROM

AMAZON.COM.Use

this link.

CCJ Publisher Rick Alan Rice dissects

the building of America in a trilogy of novels

collectively calledATWOOD. Book One explores

the development of the American West through the

lens of public policy, land planning, municipal

development, and governance as it played out in one

of the new counties of Kansas in the latter half of

the 19th Century. The novel focuses on the religious

and cultural traditions that imbued the American

Midwest with a special character that continues to

have a profound effect on American politics to this

day. Book One creates an understanding about

America's cultural foundations that is further

explored in books two and three that further trace

the historical-cultural-spiritual development of one

isolated county on the Great Plains that stands as

an icon in the development of a certain brand of

American character. That's the serious stuff viewed

from high altitude. The story itself gets down and

dirty with the supernatural, which inATWOOD

- A Toiler's Weird Odyssey of Deliveranceis the

outfall of misfires in human interactions, from the

monumental to the sublime.The

book features the epic poem"The

Toiler"as

well as artwork by New Mexico artist Richard

Padilla.

Elmore Leonard Meets Larry McMurtry

Western Crime Novel

I am

offering another novel through Amazon's Kindle

Direct Publishing service. Cooksin is the story of a criminal

syndicate that sets its sights on a ranching/farming

community in Weld County, Colorado, 1950. The

perpetrators of the criminal enterprise steal farm

equipment, slaughter cattle, and rob the personal

property of individuals whose assets have been

inventoried in advance and distributed through a

vast system of illegal commerce.

It is a ripping good

yarn, filled with suspense and intrigue. This was

designed intentionally to pay homage to the type of

creative works being produced in 1950, when the

story is set. Richard

Padilla has done his usually brilliant

work in capturing the look and feel of a certain

type of crime fiction being produced in that era.

The whole thing has the feel of those black & white

films you see on Turner Movie Classics, and the

writing will remind you a little of Elmore Leonard,

whose earliest works were westerns.

Use this link.

EXPLORE THE KINDLE

BOOK LIBRARY

If you have not explored the books

available from Amazon.com's Kindle Publishing

division you would do yourself a favor to do so. You

will find classic literature there, as well as tons

of privately published books of every kind. A lot of

it is awful, like a lot of traditionally published

books are awful, but some are truly classics. You

can get the entire collection of Shakespeare's works

for two bucks.

Amazon is the largest,

but far from the only digital publisher. You can

find similar treasure troves at

NOOK Press(the

Barnes & Noble site),Lulu,

and others.

ECONOMICS

General Motors Story

By RAR

The big walk away from GM's Super Bowl

halftime purchase of a two-minute slot, to tout their recovery as an

auto maker, was that GM is throwing their political support to the

re-election of Barack Obama. This was not, of course, the real

message of the GM commercial, but that was the message that the

political Right came away with, and the reasons are profoundly loaded

with emotional fireworks. To wit:

The "Halftime in America" theme closely

paralleled perhaps the most heralded GOP commercial spot of all

time, Ronald Reagan's "Morning

in America". It even begins with a new day dawning and it is filled

with the same romantic portrayal of American ideals, which is stuff

the Right feels it owns.

The GM spot was delivered by

Clint Eastwood, the former Mayor

of Carmel, California, who is either a Republican or a Libertarian,

depending upon the issue, but either way carries the same sort of

weight that the Republican's late icon

Charlton Heston once represented and, like Heston,

Eastwood is supposed to be theirs, not some suck-up to the

current Democratic president.

The GM yeah-us-yeah-America spot was

shown at the front-end of a presidential election year, and seemed

to break a long-standing tradition of corporations remaining neutral

regarding candidate endorsements. This, of course, comes after

some very public statements by GM executives recognizing the gratis

of the Obama Administration, and the anti-bail out rhetoric of the

political right.

Most galling of all, to

Right Wing politicos, was that the commercial seemed to them to imply

that big government bailouts of struggling corporations work!

That last one bugs the Right because whether

or not that's true depends upon whether you think your job was saved by

the $85 billion the Federal government poured into GM, in early 2009, to

keep the company afloat when it appeared that parts manufacturers and

the entire supply chain was on the verge of collapse. The Canadian

government also kicked in another $10 billion for GM's Canada Division.

Today, GM is touted as the number one auto manufacturer in the world,

regaining a title it had relinquished to Japanese automakers for some

time. GM announced $8 billion in net profits in the last year, and has

its eye on $10 billion a year, heretofore unimaginable.

The Obama Administration has made much of

the fact that the loans to GM have been paid back in full, which would

make the story one of heroic grandeur for Obama, savior of the American

Way of Life, were it more than technically true.

Only $8.7 billion of the $85 billion loaned

to GM were marked as repayable loans (and only $4.7 billion of the $10

billion loaned by the Canadians). Indeed, GM has completely returned

that money.

The majority of that huge bailout went in

share of GM stock, following a government-coordinated corporate

bankruptcy. Of the new stock, sixty-one percent was purchased by the

Federal Treasury, making every taxpaying U.S. citizen a shareholder in

GM. (Currently the Treasury owns about one-quarter of GM's stock.) Some

would call this the nationalizing of a major industry and a key stepping

stone on the path to a Socialist government.

It is sort of hard to argue with that

socialism charge, which of course comes from right wingers for whom

socialism is a blood vessel-bursting boogie man, because the once-again

wealthy GM has shown little inclination to relieve the American

taxpayer-shareholders of their economic association with GM.

According to December 2012 reports, the U.S.

Treasury owns 500 million shares of GM stock, which is valued at roughly

$10.8 billion.

You will notice that the current value of

the Treasury's stock in GM, plus the amount GM repaid as loans from the

Treasury, don't equal anything near $85 billion.

What happened to the rest of the money?

It disappeared with the falling value of GM

stock, trading at $25.95 and trending up at the time of this report

(February 9, 2012). Treasury paid $33 per share at the Initial Public

Offering in November 2010, so while the value keeps changing the U.S.

taxpayer is still on the hook for approximately $20 billion in the GM

deal. The Treasury has also written off $1.8 billion in debts from the

"old Chrysler" division of GM, and they took a beating on the sale to

Fiat of Chrysler shares owned by the U.S. and Canadian governments.

Here's the kicker: GM is sitting on $33

billion in cash - enough to buyout the shares owned by the U.S. taxpayer

and make the deal square - but it will not make that move, offering a

couple explanations. One is that they are holding on for the value of

the stock to rise, and it has shown an upward movement since the end of

2012, despite the apparent failure of the Chevrolet Volt, which had been

heralded as an important GM entry in the alternative energy market.

The other is that GM is struggling to fund a

$128 billion pension plan, and thus has another incentive to hold onto

that Treasury-owned stock for as long as possible, hoping for the

company to gain value. Spots like "Halftime in America" cannot hurt.

GM chief executive

Dan Akerson has reportedly

offered a buyback to the government, which Treasury declined on an

investment bet. Credit Suisse predicts that GM shares will rise to $32 by the November 2012

election. But what rankles the Right is that the Obama Administration

won't sell the GM shares because it is loath to

spoil its GM success story by having to report what the level of losses

would actually be if the shares were sold back to GM at their current

market value. Otherwise, GM looks a lot better on TV than it looks on

paper.

The Obama Administration strategy really

represents a high-stakes political-economic poker game using taxpayer

money. And it is far worse than it sounds in that the $33 per share the

Treasury paid in the IPO carries an actual break-even price of $53 per

share. While GM's stock value has been rising, it has been downgraded

significantly since the fourth quarter of 2011, when analysts thought it

would go as high as $42 per share, still well below the break-even mark.

This is the basic truth underlying the

Right's rage at the "Halftime in America" spot. It is warm and fuzzy,

but has little to do with the reality of our nation's economic recovery.

______

Greed Greater than Rome's

An estimated seventy percent of

the population of Rome were "slaves", in some technical or

real sense. Some were teachers, artisans, scribes, and some

were just doing hard labor. The glory of Rome was built on

the backs of exploited people, and yet the Romans were

exceedingly willing make citizens of "non-Romans". The slave

masters allowed some of their chattel to buy their freedom.

However hierarchical and

inequitable ancient Rome may have been, the infamous greed

of the Roman elite in no way compared to that of our current

Master of the Universe, defined as the investment class

globally. In ancient Rome, the top three percent of the

population controlled only 16 percent of the total wealth.

In the United States today, the top three percent control 40

percent of the nation's wealth, representing an inequality

in distribution of wealth greater than that of half the

nations of Africa.

(121211)

DAVOS:

World Economic Forum

Single Points of

Failure

Occupy Protesters at the World Economic

Forum in Davos, Switzerland.▬►

________________________

Congressional Leaders Skirting Congressional

Process

Continued from the Front Page...

The debt ceiling debacle demonstrated a fundamental principle at

work in the U.S. these days: people standing revolutionary-like on principle

regardless of its application to reality. Even Grover Norquist, whose sophomoric

oath to never raise taxes, contrived when he was barely out of high school but

now 25 years later a "contract" held with the majority of those elected to

Congress, found the idea of allowing the U.S. to default on its loans to be

ludicrous.

The

newly imagined "Super Committee" would be expected to create legislation that

would be more likely to pass votes in the House and Senate, partly because the

concept promises a 50-50 balance in spending cuts to Military and Domestic

programs. The Democrats vow to protect popular programs like Medicare and Social

Security.

The

problem is in that principle referenced above - people standing

revolutionary-like on principle regardless of its application to reality -

because pull-backs in federal funding of any kind means fewer dollars in the

system of commerce, which means less purchasing power, lower demand, cutbacks in

production and supply, reduced tax revenues, and somehow this is supposed to

eventually erase a $14 trillion debt.

The

laws governing Economics, on this level, is about as intractable as the laws of

physics. Reducing dollars in the economic system reduces the size of the system,

which shrinks the economic prospects for us all.

Currently the U.S. government is operating at about 25 percent of the country's

Gross Domestic Product while bringing in only 15 percent of GDP in revenues.

That is a gap with plenty of historic precedent that could be closed, as it has

been in the past, by two mechanisms: Federal spending on job-producing

infrastructure projects, which are in huge need of attention anyway; and levying

higher taxes on people with incomes disproportionate to those of the rest of

society.

There

is no real argument about this among thoughtful people. The problems are clear,

the solutions are tried and true. And yet, as we see with legislation on climate

change and health care and a plethora of other key issues, the power of simple

facts are failing to hold sway.

Somehow, through an extraordinary warp in the fabric of space beneath President

Barack Obama's crotch, a Democratic majority has shrunk from both houses of

Congress plus the presidency, to the presidency and the Senate, and after the

2012 elections probably nothing at all. All of this while polls seems to

indicate that the majority of public opinion is with the Democrats on most key

issues.

How can

it be? Why have Democrats, under Obama's leadership, been so utterly incapable

of playing their upper hand? Why have they ceded control of every negotiation?

I'm not sure that anyone quite understands this. For some reason a cancer has

matured in the system and infiltrated the brain. As a result of its illogical

reaction to stimuli from a variety of sources, the body is seizing. Under the

weight of this shaking, our governmental structures are crumbling, brick by

brick. In the process, an odd light of moon is being allowed to shine on what is

presently inside, and it is making everything seem pretty scary.

___________________________

Former Treasury Secretary

Lawrence Summers Discusses Confidence in an Economy and the Need for Federal

Stimulus Spending

Editor's Note:

The following is reprinted from a Reuters news release. The RCJ does not

typically reprint articles but this piece by Summers is important, largely

because it seems to be falling on deaf ears in the Obama Administration, which

is loathe to mount yet another stimulus package after blowing so much borrowed

money on financial industry bailouts. As Summers' article points out,

over-confidence created the economic overreach that further created the housing

bubble that burst in 2006. A resulting lack of public confidence can create a

long period of recession, such as that experienced in Japan after a similar

economic bubble, and the only way to avert a catastrophic lost decade of

American economic vitality is to rebuild public confidence through job-producing

stimulus programs. The obvious place to spend is on the U.S.' aged and ragged

infrastructure. And, as Summers points out, the time to do it is now, when

interest rates are at historic lows.

By Lawrence H. Summers

CAMBRIDGE, Mass., June 12, 2011 (Reuters) - Even

with the massive 2008-2009 policy effort that successfully prevented financial

collapse and depression, the United States is now halfway to a lost economic

decade.

Over the last five years, from the first quarter of 2006

to the first quarter of 2011, the U.S. economy's growth rate averaged less than

1 percent a year, about like Japan during the period when its bubble burst. At

the same time, the fraction of the population working has fallen from 63.1

percent to 58.4 percent, reducing the number of those with jobs by more than 10

million. The fraction of the population working remains almost exactly at its

recession trough and recent reports suggest that growth is slowing.

Beyond the lack of jobs and incomes, an economy producing

below its potential for a prolonged interval sacrifices its future. To an extent

that once would have been unimaginable, new college graduates are this month

moving back in with their parents because they have no job or means of support.

Strapped school districts across the country are cutting out advanced courses in

math and science and in some cases only opening school four days a week. And

reduced incomes and tax collections at present and in the future are the most

important cause of unacceptable budget deficits at present and in the future.

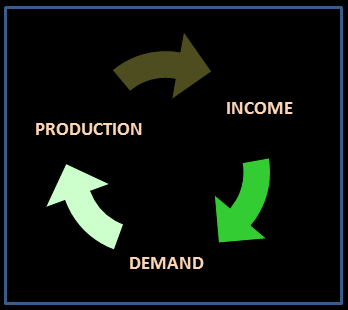

You cannot prescribe for a malady unless

you diagnose it accurately and understand its causes. Recessions are times when

there is too little demand for the products of businesses, and so they fail to

employ all those who want to work. That the problem in a period of high

unemployment like the present one is a lack of business demand for employees,

not any lack of desire to work is all but self-evident. It is demonstrated by

the observations that (i) the propensity of workers to quit jobs and the level

of job openings are at near-record low levels; (ii) rises in nonemployment have

taken place among essentially all demographic skill and education groups; and

(iii) rising rates of profit and falling rates of wage growth suggest that it is

employers, not workers, who have the power in almost every market.

I belabor the idea that lack of demand is the fundamental

cause of economies producing below their potential because the failure to

recognize the centrality of demand can have catastrophic consequences. But for

Hitler and the military buildup up he caused, FDR would have left office in

early 1941 a failure, with American unemployment above 15 percent and with the

recovery promise of the New Deal shattered by the premature attempt in 1937 to

reassert the traditional virtues of deficit reduction and inflation control.

When I entered the Clinton administration in 1993, it was generally believed

that Japan had the potential to grow its economy by 4 percent a year going

forward, enough to have doubled output from that time until now. Instead output

has barely grown, a consequence of the post bubble stagnation that Japan

suffered.

A sick economy constrained by demand works

very differently than a normal one. Measures that usually promote growth and job

creation can have little effect or can actually backfire. When demand is

constraining an economy, there is little to be gained from increasing potential

supply.

In a recession, if more people seek to borrow less or save

more, there is reduced demand and hence fewer jobs. Training programs or

measures to increase work incentives for those with both high and low incomes

may affect who gets the jobs, but in a demand-constrained economy will not

affect the total number of jobs. Most paradoxically, measures that increase

productivity and efficiency, if they do not also translate into increased

demand, may actually reduce the number of people working as the level of total

output remains demand constrained.

Traditionally, the American economy has recovered robustly

from recession as demand has been quickly renewed. Within a couple of years

after the only two deep recessions of the post-World War II period -- those of

1974-1975 and 1980-1982 -- the economy was growing in the range of 6 percent or

more -- rates that seem inconceivable today. Why?

Inflation dynamics defined the traditional post-war

American business cycle. Recoveries continued and sometimes even accelerated

until they were murdered by the Federal Reserve with inflation control as the

motive. When the Fed became concerned about inflation accelerating, usually too

late, it raised interest rates and crunched credit, stifling housing, business

investment, and consumer durable purchases and causing the economy to go into

recession. After inflation slowed, rapid recovery propelled by dramatic

reductions in interest rates and a backlog of deferred investment was almost

inevitable.

Our current situation is very different.

With more prudent monetary policies, expansions are no longer cut short by

rising inflation and the Fed hitting the brakes. All three American expansions

since Paul Volcker brought inflation back under control have run long. They end

after a period of overconfidence drives the prices of capital assets too high

and the apparent increases in wealth give rise to excessive borrowing, lending

and spending.

After bubbles burst, there is no pent-up desire to invest.

Instead, there is a glut of capital caused by overinvestment during the period

of confidence: vacant houses, malls without tenants, and factories without

customers. At the same time, consumers discover that they have less wealth than

they expected, less collateral to borrow against and are under more pressure

than they expected from their creditors. Little wonder that private spending

collapses and that post-bubble economic downturns often last more than a decade

and are only ended through external events like military buildups.

Pressure on private spending is enhanced by structural

changes. Take as a vivid example the publishing industry. As local bookstores

have given way to megastores, megastores have given way to Internet retailers,

and Internet retailers have given way to ebooks, two things have happened. The

economy's productive potential has increased and its ability to generate demand

that fulfills the potential has been compromised as resources have been

transferred from middle-class retail and wholesale workers with a high

propensity to spend up the scale to those with a much lower propensity to spend.

And the need for capital investment in distribution networks has come down.

What then is to be done? This is no time

for fatalism or for traditional political agendas that the two parties have

pushed in more normal times. The central irony of financial crisis is that while

it is caused by too much confidence, borrowing and lending, and spending, it is

only resolved by increases in confidence, borrowing and lending, and spending.

It follows that the central objective of national economic policy until

sustained recovery is firmly established must be increasing confidence,

borrowing and lending, and spending. Unless and until this is done, other

policies, no matter how apparently appealing or effective in normal times, will

be futile at best.

We should recognize that it is a false economy to defer

infrastructure maintenance and replacement, and instead take advantage of a

moment when 10-year interest rates are below 3 percent and construction

unemployment approaches 20 percent to expand infrastructure investment.

It is far too soon for financial policy to

shift toward preventing future bubbles and possible inflation and away from

assuring adequate demand. The underlying rate of inflation is still trending

downward, and the problems of insufficient borrowing and investing exceed any

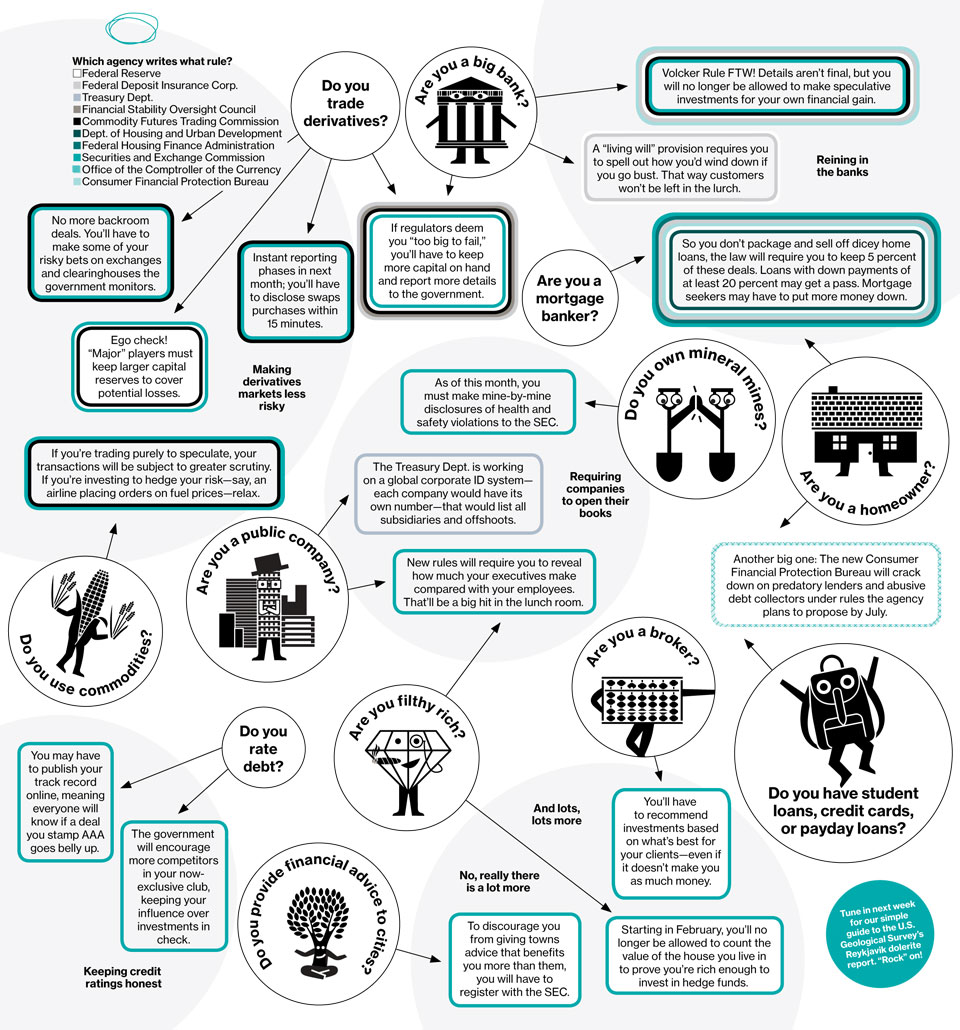

problems of overconfidence. The Dodd-Frank legislation is a broadly appropriate

response to the hugely important challenge of preventing any recurrence of the

events of 2008. It needs to be vigorously implemented. But under-, not

over-confidence is the problem of the moment and needs to be the focus of

policy.

Most important, the fiscal debate needs to take on board

the reality that the greatest threat to the nation's creditworthiness is a

sustained period of slow growth that, as in southern Europe, causes debt-GDP

ratios to soar. This means that essential discussions about medium-term measures

to restrain spending and raise revenues need to be coupled with a focus on

near-term growth. Without the payroll tax cuts and unemployment insurance

negotiated by the president and Congress last fall we might well be looking

today at the possibility of a double dip. Substantial withdrawal of fiscal

support for demand at the end of 2011 would be premature. Fiscal support should

be continued and indeed expanded by providing the payroll tax cut to employers

as well as employees. Raising the share of the payroll tax cut from 2 percent to

3 percent would be desirable as well. At a near-term cost of a little over $200

billion, these measures offer the prospect of significant improvement in

economic performance over the next few years translating into significant

increases in the tax base and reductions in necessary government outlays.

It is appropriate that policy in other dimensions be

informed by the shortage of demand that is a defining characteristic of our

economy. For example, the Obama administration is doing important work in

promoting export growth by modernizing export controls, promoting U.S. products

abroad and reaching and enforcing trade agreements. Much more could be done

through changes in visa policy, for example, to promote exports of tourism as

well as education and health services. In a similar vein, recent presidential

directives regarding relaxation of inappropriate regulatory burdens should be

rigorously implemented to boost confidence.

Perhaps the most fundamental strength of the United States

is its resilience. We averted Depression by acting decisively in 2008 and 2009.

Now we can avert a lost decade by recognizing current economic reality.

(Lawrence H. Summers is the Charles W. Eliot

University Professor at Harvard University and a former U.S. Treasury secretary.

He speaks and consults widely on economic and financial issues.) (Editing by

Jonathan Oatis)

Copyright 2011 Thomson Reuters

By RAR

As

this year's World Economic Forum(WEF) drew to a close on

Saturday (01/28/12), the world's wealthiest people were

expressing concern about the global financial situation. Keynote

speaker and Hong Kong business leader

Donald Tsang stated flatly - "I've never been as

scared as now about the world, what is happening in Europe."

What is happening in Europe is the

collapse of the economy of Greece, despite several

European Economic Union (EEU)

plans to keep the country from defaulting on its government

debts. This would almost certainly set off a domino effect

putting the wobbly economies of Italy and Spain into default.

The problem, as Tsang states, is

that "We do not know how deep this hole will be when the whole

thing implodes on us." And he adds: "Nobody is immune."

INDICTMENT

OF IN-SOLIDARITY: That last warning shot ("Nobody is

immune") is an indictment of a world economic "community" that

let Asian economies, that bubbled and then imploded in 1990s,

struggle out of disaster on their own, a memory for Tsang that

has left scars. Tsang's point to the economic leaders of the

world was that "In Europe now, you need decisive action, you

need overkill. You need to inspire confidence. That confidence

must come in the decisive action of government, working

together. And do it quickly."

Tsang is freaked out because the

17-nation EEU has not come up with a bailout scheme of

sufficient proportion to do more than prop up Greece to stall

its complete collapse. It turns out that the 17 nations -- each

with their own histories, cultures and, previous to the

invention of the "Euro", their own currencies -- are remarkably

reluctant to suddenly begin acting as one. They are reluctantly

committed to the promise of association with a large,

benefit-sharing union, but not so much to the responsibility

that membership confers.

A big part of the reason for that is

that all of these nations are in trouble themselves, and

while many are not in the desperate economic conditions of

Greece, Italy and Spain, that are also not really in a strong

enough economic position to help.

The governments of the world are at

cross purposes, and sharing only one common trait: they are no

longer in control of their fates.

CORPORATIZATION: The world economy is

staggeringly different now from even a time in history as recent

as the 1990s. The global financial system is now so

interconnected that any protective buffers enjoyed by the

earlier, smaller economies of individual nations are largely

gone.

Cato Institute associate Tom G.

Palmer has notably defined globalization as "the diminution or

elimination of state-enforced restrictions on exchanges across

borders and the increasingly integrated and complex global

system of production and exchange that has emerged as a result."

Otherwise put, we are now realizing

the early harvests of a global deregulation that has allowed

wealthy corporations to shift their jobs and accounting

practices to those parts of the world that ensure the best

return for their investors without regard for national

allegiance. Government, the mantra goes, are intrusive and

burdensome and do not produce economic benefits in the form of

jobs, only treasury-draining social welfare.

Government debates aside, investors

and consumers have become intoxicated with the products of the

digital age, the existence of which are reinventing the way

users interact with one another and manage their affairs. To

make this happen, the corporate giants have set price points on

products that can only be made profitable by minimizing labor

and materials overheads, which are achievable only by

outsourcing to low-cost manufacturers in Asia and other

developing nations.

That price-pointing factor, which

makes it possible for the working poor of the developed world to

justify the purchase of iPhones and other electronic products,

also makes it impossible for more than a few companies to

compete, effectively creating a monopoly on whole groups of

products that are now indispensable in the age the products

themselves have created. This is true not only for electronics,

but for brand-name consumer products in general.

This has been a neat trick of

commercial evolution that is having devastating effects on the

world it is reshaping, as might be expected when changes are

taking place with rapidity unparalleled in all of human history.

ECONOMIC IRONY:

While the perceptions of most people would be that the world of

today has gotten smaller, and people have probably become

more sensitized to the living conditions of populations around

the world, this has not translated into government policies that

could be construed as responsive to the global community.

Quite the contrary, stewardship has

been rested from governments by virtue of their inability to

finance fiduciary burdens. Tax revenues have collapsed with

global deregulation, and with them have collapsed the power of

governments to do anything other than engage in conflict. With

control of the economy ceded to international corporate powers,

building weapons and putting poor people in uniforms is about

the only certain job creation scheme that governments have left

at their disposal, and it is among the last available

expressions of nationalism.

The world seems on a collision

course with itself, and in a period in which the temptation to

isolate personal interests, from the ravages of a world beyond

control, is strong indeed.

Deregulation has allowed this

transition of power from governments to a few wealthy

corporations, and a relative handful of ultra-wealthy

stakeholders (the Davos WEF folks). The fruits of deregulation

are a series of single point failures, put in place by

the consolidation of wealth into a very few bank accounts

worldwide - and they are not the bank accounts of the

people viz a vie their governments.

As Donald Tsang ranted (some say) in

his WEF address, the output of globalization confers no

protection for anyone. He wondered aloud, as reported by The

Huffington Post, about the health of financial institutions

that trade with Hong Kong's banks and the potential for trouble

rippling out from the Euro zone.

Will governments fall one by one? First Greece,

then Italy, then Spain. Will it mean trouble for leveraged investors in Hong

Kong? And where will it stop? Or will it stop at all?

Perhaps the "1 Percent" are remaking the world to

their liking, paying believers and hucksters on all sides of the political aisle

to flout their philosophy that promises that some will be kings, even as the

well-being of most of us will continue to decline. As Tsang pointedly

discovered, individual actors are not inclined to come to the aid of other

actors, particularly if not doing anything, like sharing their debt load, yields

a perceived advantage over the distressed.

Corporations are not really people, that's what

governments are. It is people who are in trouble in Greece and Italy and Spain,

and we live in a time out of sync with human need, and more in line with the

needs of "the job creators".

They are like gods to us now, that jobs are so

few and mean so much. We'll work for half of what we used to, if that's what it

will take to just be employed. And we will be employed, when finally

wages have been reduced to the point that it will be cheaper and more cost

effective for corporations to bring their manufacturing operations back home,

where there is cheap labor to exploit. And once government protections have been

so eviscerated that corporations are free to behave as they want.

RARWRITER PUBLISHING GROUP PRESENTS

RARWRITER PUBLISHING GROUP PRESENTS